When considering an overseas secondment to the United Kingdom you must first give consideration as to what your tax implications are in the UK and the country you are leaving.

The questions to consider:

How long is the secondment for?

Is your family to travel with you, or remain behind?

Will I remain a tax resident in my country of residence?

Will I continue to remain an employee of my current employer?

Am I to transfer to the overseas employing office and if so, what are the terms?

Will I be a UK tax resident, if so am I eligible to claim split year treatment?

Do I qualify for the Remittance Basis of accounting?

Does the UK have a double taxation agreement with my country of residence?

Your tax residency is fundamental to determine who has taxing rights over your worldwide income with particular reference to the salary being offered to you.

Your residency is often a significant issue, as residents of the UK are subject to income tax on their worldwide income, unless remittance basis claimed and non-residents are only taxable on their UK sourced income subject to the exempted income provisions.

It is possible to be a dual resident with the overseas country and the UK. Should this be the case you would need to consider which country has overriding residency which is commonly referred to as treaty residency as it is the conditions set in the double taxation agreement which would determine this deciding point.

Once your residency position has been determined you can better understand who has taxing rights over your income along with your tax reporting obligations in both countries.

As a non-resident for Australian tax purposes you will be required to lodge an Australian tax return with the Australian Taxation Office (ATO) to report your Australian sourced income & gains.

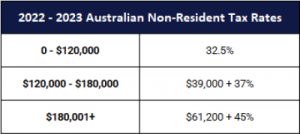

Your income is taxed at non-resident rates of tax (32.5% on the first $120,000 (2022/2023) and you are not entitled to the tax free threshold ($18,200 for 2022/2023).

The Australian tax year runs from 1st July to 30th June.

You will need to apply for a tax file number in order to lodge an Australian Tax Return if you do not already have a TFN and you have an obligation to lodge.

Should you have an outstanding HELP debt then you are also required to report your overseas earnings on an Australian tax return and make any repayments due.

As a non-resident for Australian tax purposes living in Hong Kong you will be required to lodge an Australian tax return with the Australian Taxation Office (ATO) to report your Australian sourced income & gains.

Should you have an outstanding HELP debt then you are also required to report your overseas earnings on an Australian tax return and make any repayments due.

Your income is taxed at non-resident rates of tax (32.5% on the first $120,000 (2022/2023)and you are not entitled to the tax free threshold ($18,200 for (2022/2023).

The Australian tax year runs from 1st July to 30th June.

You will need to apply for a tax file number in order to lodge an Australian Tax Return if you do not already have a TFN and you have an obligation to lodge.

As a non-resident for Australian tax purposes you will be required to lodge an Australian tax return with the Australian Taxation Office (ATO) to report your Australian sourced income & gains.

Your income is taxed at non-resident rates of tax (32.5% on the first $120,000 (2022/2023)and you are not entitled to the tax free threshold ($18,200 for 2022/2023).

The Australian tax year runs from 1st July to 30th June.

You will need to apply for a tax file number in order to lodge an Australian Tax Return if you do not already have a TFN and you have an obligation to lodge.

Should you have an outstanding HELP debt then you are also required to report your overseas earnings on an Australian tax return and make any repayments due.